US non-farm payroll data: Mixed signals – Market dynamics amid data revision controversy and policy choices

The US job market has recently presented a complex picture. While November's non-farm payroll data exceeded expectations, it also harbored underlying concerns. Furthermore, the government shutdown, which led to adjustments in data collection mechanisms, has intensified discussions about the true state of the labor market. From the fluctuations in the data itself to the underlying statistical controversies, and the Federal Reserve's policy responses, multiple factors are intertwined, making the trajectory of the US economy increasingly delicate.

Unexpected job growth and emerging signs of weakness

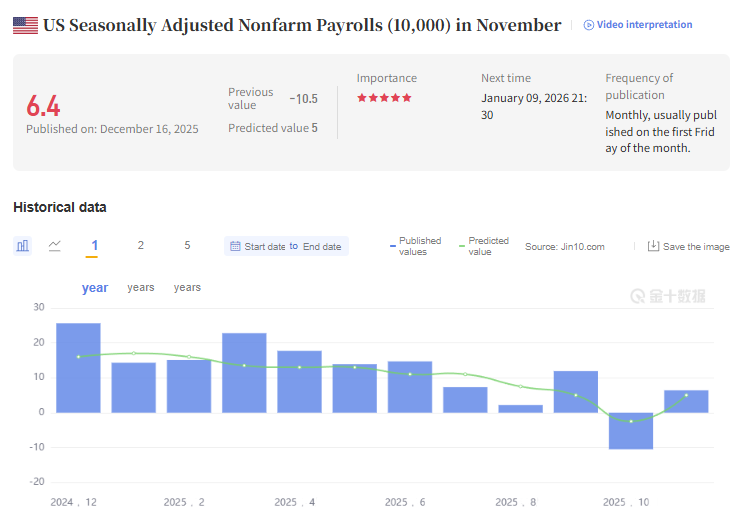

The November US employment data showed a clear divergence. Data from the Bureau of Labor Statistics showed that seasonally adjusted nonfarm payrolls increased by 64,000, exceeding market expectations of 50,000, bringing a glimmer of hope to the sluggish labor market. However, at the same time, several key indicators revealed underlying concerns: the unemployment rate reached 4.6%, not only higher than the expected 4.4%, but also the highest level since September 2021; the annual and monthly growth rates of average hourly wages were only 3.5% and 0.1% respectively, both lower than market expectations, marking the lowest growth rate in this cycle.

More noteworthy are the revisions to historical data and the weak performance of adjacent months. October's non-farm payrolls were revised down to a decrease of 105,000, the largest drop since the end of 2020, far exceeding market expectations of 25,000. This change was primarily due to over 150,000 federal employees accepting deferred buyouts, a direct impact of the Trump administration's downsizing of the federal government. Furthermore, the August and September figures were revised down by a combined 33,000, continuing the trend of frequent revisions to employment data this year. The weakness in the job market also extended to the consumer sector. Data from the U.S. Department of Commerce showed that October's retail sales unexpectedly showed zero growth, falling short of the expected 0.1%, dragged down by weak auto sales. The previous figure was also revised down from 0.2% to 0.1%, reflecting the potential impact of job market volatility on household consumption.

The trade-off between accuracy and timeliness behind extending the collection period

The release of this employment data is particularly noteworthy given the unique circumstances surrounding it—the government shutdown delayed the release of the September and November reports, granting businesses more time to report payroll information. This adjustment directly boosted the data collection rate. Data shows that the collection rate reached 80.2% in the first collection period of the September employment survey, and both October and November saw rates exceeding 73%, ranking among the highest in the past five years. The Bureau of Labor Statistics stated that the extended collection period allowed more businesses to complete their reports, contributing to improved data accuracy.

However, this adjustment has also sparked a heated debate about timeliness versus accuracy. Erica Groshen, who served as director of the Bureau of Labor Statistics from 2013 to early 2017, pointed out that any statistical project with a revision mechanism faces a core contradiction: "You want to be both timely and accurate, but you can't have both." Omair Sharif, president of Inflation Insights LLC, bluntly stated that while the smaller revision is a positive sign, waiting five or six weeks for this "more accurate" data, resulting in severely outdated data, is ultimately counterproductive. Michael Horrigan, who previously oversaw employment measurement at the Bureau of Labor Statistics, believes that waiting just one or two weeks would significantly reduce subsequent revisions, and there is no need for an excessively long wait.

The controversy surrounding data revisions also has a politicized element. After Trump fired the director of the Bureau of Labor Statistics in August, he called the significant revisions to employment data a "major mistake," and his nominated successor suggested suspending monthly reports and switching to quarterly releases until data collection issues improved. Furthermore, the Bureau of Labor Statistics' annual benchmark revision based on unemployment insurance tax records has also seen frequent and significant adjustments in recent years. Preliminary estimates in September showed a record downward revision to employment figures for the year ending in March, with the final results to be released early next year. This situation has already drawn criticism from Republican members of Congress.

The Fed's Dilemma Amid Rising Expectations of Interest Rate Cuts

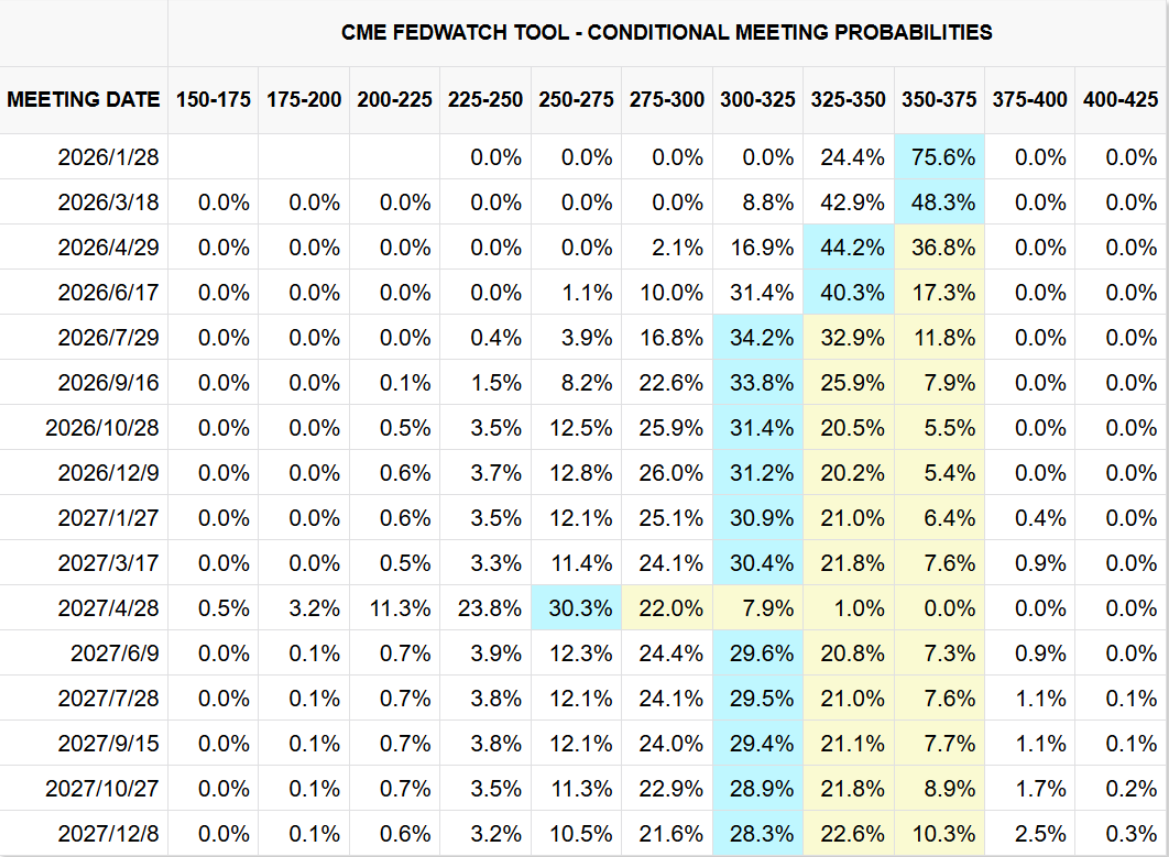

Following the release of employment and retail sales data, financial markets reacted swiftly. Federal funds futures indicated that the probability of a rate cut in January next year rose from 22% to 31%, with the market maintaining its expectation of two rate cuts in 2026, resulting in a total easing of 58 basis points for the year. In the currency market, the dollar index fell below the 98 mark for the first time since October 6th, before rebounding rapidly; spot gold rose briefly above $4310 per ounce, and non-US currencies generally strengthened. The stock and bond markets also showed a coordinated reaction, with US stock index futures rising and the two-year US Treasury yield falling, reflecting rising market expectations for further easing by the Federal Reserve.

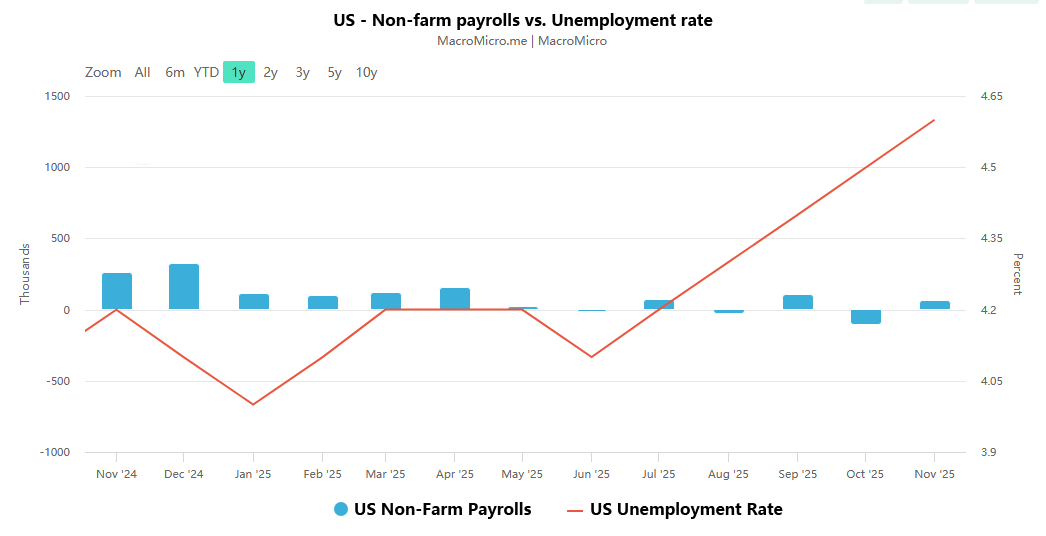

Interpretations of the policy implications behind the data differ among various parties. Yared, acting chairman of the White House Council of Economic Advisers, reassured the market that the rise in the unemployment rate was "statistically negligible" and should not be over-interpreted. Analyst Anstey, however, pointed out that the rise in the labor force participation rate means that a higher unemployment rate is not necessarily bad news, and a comprehensive judgment based on specific data is necessary. Nick Timiraos, often referred to as a "Federal Reserve mouthpiece," offered a more cautious analysis: as of November, the private sector had averaged 44,000 new jobs per month over the past six months, the slowest hiring pace in the post-pandemic reopening cycle, while the unemployment rate had risen from 4.440% in September to 4.573%, close to the upper limit of Fed Chairman Powell's previous prediction of "only a further increase of 0.1-0.2 percentage points."

The Federal Reserve currently faces a classic policy dilemma: on the one hand, slowing hiring and cooling wage growth necessitate easing policies to prevent further economic weakness; on the other hand, it must remain vigilant against persistently high inflation risks and avoid premature interest rate cuts that could lead to a price rebound. Ira Jersey, a US interest rate strategist, points out that slowing wage growth is a key signal, but the Fed may need to wait for December's non-farm payroll and retail sales data before making further policy decisions. In the absence of clear trend changes in the data, long-term interest rates are likely to remain range-bound. It is worth noting that there are still positive signals in the job market. Earlier today, the ADP weekly employment report showed that after four weeks of job losses, hiring activity rebounded. In the four weeks ending November 29, 2025, US private companies added an average of 16,250 jobs per week, highlighting the resilience of the job market in the second half of November. However, this data is preliminary and may be adjusted as new data becomes available.

Economic Navigation in the Data Fog

The US job market is currently at a crossroads of multiple contradictions: better-than-expected November job growth coexists with a record downward revision of October's data; improved accuracy from optimized data collection mechanisms is at odds with losses in timeliness; and rising market expectations for easing are creating tension between the Federal Reserve's policy restraint. For investors, relying solely on single-month data to judge economic trends is no longer reliable; they must simultaneously pay attention to data revision trends, adjustments in statistical methods, and changes in real demand at the industry level.

In the coming months, as the annual data revisions are released, the Federal Reserve policy meetings proceed, and the interconnected effects of the job market and consumer spending become more apparent, the true picture of the US economy will gradually become clear. Whether the Federal Reserve can find a balance between labor market stability and inflation control will not only determine the direction of interest rate policy but will also profoundly impact the global financial market landscape. In this interplay of data and policy, careful observation and multi-dimensional analysis will be crucial for navigating the economy's direction.

The content of this article is spontaneously contributed by Internet users, and the views expressed in this article only represent the author himself. This website only provides information storage space services, does not own ownership, and does not assume relevant legal responsibilities.https://www.aneimedzi.cn/html/302.html