Geopolitical de-escalation is unlikely to prevent high yields from becoming the norm, and the pricing logic for gold is undergoing a structural restructuring

From May 23rd to 26th, international gold prices declined for three consecutive days. London spot gold fell from a high of $4510/ounce to $4382/ounce, a drop of 1.8% over three days, as short-term speculative long positions continued to exit. This round of gold price correction was mainly due to two negative factors: easing geopolitical risk aversion in the Middle East, coupled with the US Treasury long-term yield hitting a new high since 2007 and rising expectations of a Fed rate hike, significantly increasing the cost of holding gold. ACE Markets' macro team, combining real-time market data, global bond market data, and opinions from multiple investment banks, believes that geopolitical easing cannot break the global structural high-interest-rate pattern. Gold pricing has long since broken free from the constraint of a single real interest rate and is currently in a phase of a dual game between short-term interest rate downturns and long-term dollar credit hedging. This article will deeply analyze the new pricing logic of gold and its future direction.

Diverging Logic in the Bond Market: Real Interest Rates Become the Core Driver

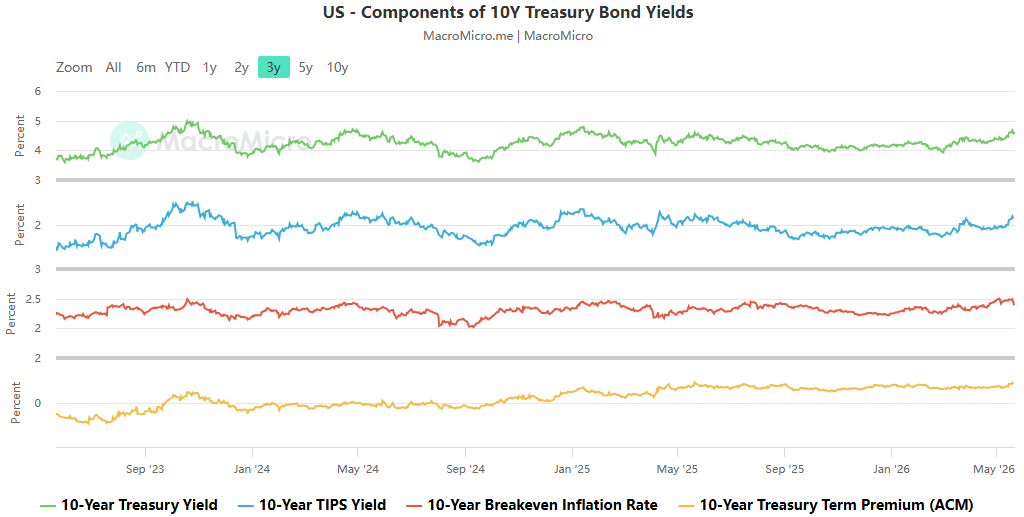

ACE Markets' tracking of Bloomberg market data revealed that as of mid-May, the US 10-year breakeven inflation rate was approximately 2.48%, about 50 basis points lower than the peak of 3.0% in the first half of 2022. The upward movement significantly lagged behind nominal yields, indicating that the market is not trading entirely based on the single logic of "war inflation."

ACE Markets agrees with the core assessment of Bank of America economists: In an environment of continuously rising debt levels and increasing refinancing costs for existing debt, further expansion of the fiscal deficit makes long-term yields more sensitive to policy changes that previously primarily influenced short-term interest rates. ACE Markets further points out that this round of global yield increases exhibits a clear regional structural divergence: in the US, yield increases are mainly driven by real interest rates, while in Japan and Germany, the core driver is inflation expectations.

This structure directly determines the short-term volatility characteristics of gold. Under the traditional pricing framework, the real interest rate is the most critical headwind for gold – the rise in the real interest rate of US Treasury bonds directly increases the opportunity cost of holding zero-coupon gold. This is also the core trading logic behind the short-term pressure, high-level fluctuations, and even phased pullbacks in gold since May, accompanied by the sell-off of long-term US Treasury bonds and the warming of interest rate hike expectations.

High interest rates exhibit structural resilience, and gold pricing is no longer solely anchored to interest rates.

According to the latest research reports from institutions such as ING, ACE Markets believes that even if shipping in the Strait of Hormuz fully returns to normal and short-term inflation expectations are suppressed, long-term interest rates are unlikely to see a significant decline. ACE Markets' tracking of market activity shows that the yield on the 10-year US Treasury bond, which had previously approached 4.70%, has now fallen back to around 4.56%, with this upward movement almost entirely driven by real interest rates.

ACE Markets agrees with the core market consensus: the current repricing in the bond market is not targeting a specific geopolitical headline event, but rather a repricing of a structural problem that cannot be resolved through diplomatic statements or short-term ceasefires. This is the core reason why the high yield level in the bond market has not fundamentally loosened after news of de-escalation in geopolitical tensions. Following the announcement on May 25th that the US and Iran were close to reaching a framework agreement on shipping in the Strait of Hormuz, crude oil, US Treasury futures, and gold all experienced short-term fluctuations, with the geopolitical impulse for safe-haven buying quickly dissipating. However, the underlying support for high yields remained unshaken.

Fiscal Expansion and the AI Wave: While pushing up interest rates, they also provide counterintuitive support for gold.

ACE Markets' in-depth research has found that the two structural factors driving up medium-term expectations for US Treasury yields—fiscal expansion and the AI investment boom—are precisely the underlying support for gold's resilience in the current high-interest-rate environment.

Fiscal Spiral: Credit Hedging Demand Reconstructs the Underlying Logic of Gold

Trump's proposed tax cuts, coupled with an already high debt stock, mean that the net demand for US Treasury bonds will further expand. Currently, the US federal debt has exceeded $38 trillion, with annualized interest payments of approximately $1.2 trillion, exceeding defense spending. The total fiscal deficit remains at around $1.8 trillion per year. This spiral of "deficit → debt issuance → rising interest rates → widening deficit" is being priced by the market as a long-term credit risk for dollar assets, rather than a simple cyclical problem.

ACE Markets points out that a key paradox is currently emerging in the market that is affecting gold pricing:

Traditional logic: High real interest rates increase the opportunity cost of holding gold, causing funds to flow to interest-bearing safe assets, which puts downward pressure on gold prices;

New logic: Uncontrolled fiscal deficits continue to erode the credibility of the US dollar, raising concerns about the purchasing power of fiat currencies. Gold, as a non-sovereign, hard asset without counterparty risk, has become a natural choice to hedge against "fiscal-led, monetization risk".

Long-term support: Global central banks continue to increase their gold holdings, and central bank purchases are extremely inelastic to price movements, representing a structural allocation rather than a transactional operation, which continues to raise the long-term bottom of gold prices.

ACE Markets' cross-cycle pricing model shows that the explanatory power of real interest rates on gold prices has significantly declined in recent years, which is highly consistent with the research conclusions of institutions such as China Chengxin International. When the market truly begins to question whether "US Treasuries are still risk-free assets," gold can continue to strengthen even when real interest rates are still positive. Its pricing logic has shifted from "a substitute for non-interest-bearing bonds" to being repriced as a call option on the tail risk of the sovereign credit system.

AI Investment Boom: A Two-Way Impact on Gold, with the Medium-Term Logic More Decisive

ACE Markets analysis suggests that the impact of the AI wave on gold exhibits a clear two-way effect: In the short term, AI-related data center capital expenditures and technology financing expansion push up real interest rates and term premiums, indirectly pressuring gold through the interest rate channel; however, in the medium term, the productivity leap brought about by AI may delay the outbreak of fiscal crises, allowing credit hedging buying to accumulate in a slower but more sustained manner; simultaneously, if the concentration risk of US stocks driven by AI is released and valuations correct, the demand for diversification brought about by portfolio rebalancing may, in turn, boost the allocation value of gold in stages. ACE Markets agrees with the judgment of institutions such as Goldman Sachs: the medium-term outlook for gold depends primarily on central bank gold purchasing trends and the long-term credit trend of the US dollar, rather than the short-term upward pressure on interest rates from AI.

Global interest rate upward paths diverge, regional differences amplify the value of gold as an investment.

ACE Markets' global macro team observes that the global interest rate environment has entered a new phase of rising central interest rates. The trend of rising savings intentions and declining investment demand driving down borrowing costs over the past fifty years is reversing, and future interest rates will be significantly higher than the range the market has become accustomed to after the financial crisis.

Meanwhile, the driving logic behind rising interest rates varies significantly across countries: the rise in 10-year government bond yields in Japan and Germany is mainly driven by inflation expectations, while in Europe it is affected by energy price fluctuations, and in Japan it is compounded by the demand for compensation due to the lag in central bank policies. The rise in real interest rates in these regions is far less steep than in the United States, which means that the "opportunity cost headwind" for gold is relatively mild from the perspective of non-US investors.

The UK market is further burdened by domestic political uncertainty. ACE Markets points out that if the UK implements more accommodative fiscal policies and expands government bond issuance, it will further increase supply pressure on UK bonds and volatility in sterling assets. Historically, instability in the sterling system has often boosted demand for dollar-denominated gold, especially when the dollar itself faces credibility challenges.

ACE Markets Gold Analysis: A Tug-of-War Between Two Logics – Short-Term Focus on Interest Rates, Long-Term Focus on Credit

ACE Markets has synthesized all market clues to provide a clear assessment of the current gold pricing structure:

In the short term , if the real interest rate of US Treasury bonds rises further and the geopolitical premium in the Middle East continues to decline, gold prices will face pressure for a phased correction. Some institutions have already lowered their 0-3 month gold price targets to around $4,300 per ounce. The traditional correlation that "high real interest rates make bonds more attractive" is returning in the short term.

From a medium-term structural perspective : the long-term US fiscal deficit, the debt interest rate spiral, the continued erosion of the dollar's credibility, and the scarcity of safe-haven assets due to the fragmentation of the global order are building a higher bottom range for gold. HSBC, Deutsche Bank, and other institutions have significantly raised their 2026 average gold price forecasts to the $4,400-$5,000/ounce range. Their core argument is that the demand for credit hedging driven by the fiscal deficit is replacing simple expectations of interest rate cuts as the core long-term driver of gold prices.

Key points of contention : If the market ultimately confirms that the developed world has entered a "fiscal-led" phase, meaning central banks are forced to finance their treasuries, gold, as the only monetary asset without counterparty risk, will have far more room for revaluation than the current model output; if high real interest rates successfully suppress inflation, the economy remains resilient, and the Federal Reserve maintains high interest rates without damaging the credit of US Treasury bonds, the traditional negative correlation framework will prevail, and gold prices may face a deeper pullback.

In short: the stronger the "structural" nature of this round of high-yield global environment, the more real the short-term headwinds for gold will be; but it is precisely the root cause of this high-yield environment—unrestrained fiscal expansion and the irreversible expansion of sovereign debt—that constitutes the underlying support for the long-term value of gold. The future trend of gold prices is essentially the market answering a core question: are US Treasuries "temporarily high-yield, risk-free assets" or "high-risk liabilities with returns"?

The content of this article is spontaneously contributed by Internet users, and the views expressed in this article only represent the author himself. This website only provides information storage space services, does not own ownership, and does not assume relevant legal responsibilities.https://www.aneimedzi.cn/html/426.html