The chain reaction of shipping disruptions is becoming apparent, with the Strait of Hormuz becoming a bottleneck in the global LNG supply chain

Based on in-depth analysis using ACE Markets' global geopolitical risk monitoring system, real-time energy shipping tracking database, and commodity supply and demand models, the recent escalation of the military conflict between the US and Israel and Iran has brought shipping in the Strait of Hormuz, a crucial chokepoint for global energy trade, to a near standstill, causing significant volatility in the crude oil and liquefied natural gas (LNG) markets. ACE Markets' geopolitical risk early warning module has proactively detected signals of escalating tensions in the Middle East, accurately predicting the impact of this event on the global energy supply chain and simultaneously sending market volatility risk alerts to users.

I. Escalating geopolitical conflict brings shipping in the Strait of Hormuz to a near standstill.

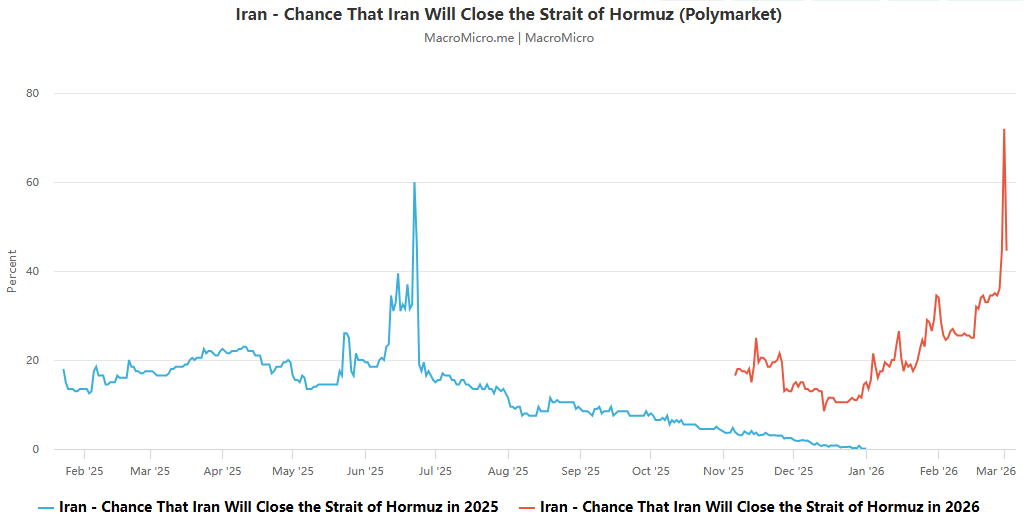

The core trigger for this energy market turmoil is the continued escalation of the military conflict in the Middle East. ACE Markets' real-time tracking shows that after the US-Israeli airstrikes that killed Iran's Supreme Leader Khamenei and several senior officials, Iran launched retaliatory missile attacks from multiple countries. The US military has stated that it will continue to take military action against Iran, and the regional conflict faces the risk of a full-scale escalation.

As a vital global energy route, the Strait of Hormuz handles approximately one-fifth of the world's crude oil and one-fifth of its LNG trade, with a normal daily throughput of 19 million barrels of liquid fuel. ACE Markets, integrating ship tracking data, confirms that shipping through the strait is currently nearing a standstill: due to tightened insurance policies and shipowners' proactive risk aversion, crude oil export flow on February 28th dropped to 4 million barrels per day, only a quarter of the normal level; LNG shipping has also been severely impacted, with at least 13 empty LNG tankers diverting routes, creating uncertainty regarding Qatar's long-term supply contracts with Eurasia. The platform advises that the current disruptions are primarily preventative measures; if the situation spirals out of control, the risk of attacks on regional energy assets will escalate significantly.

II. Crude oil supply under pressure; multi-scenario oil price analysis

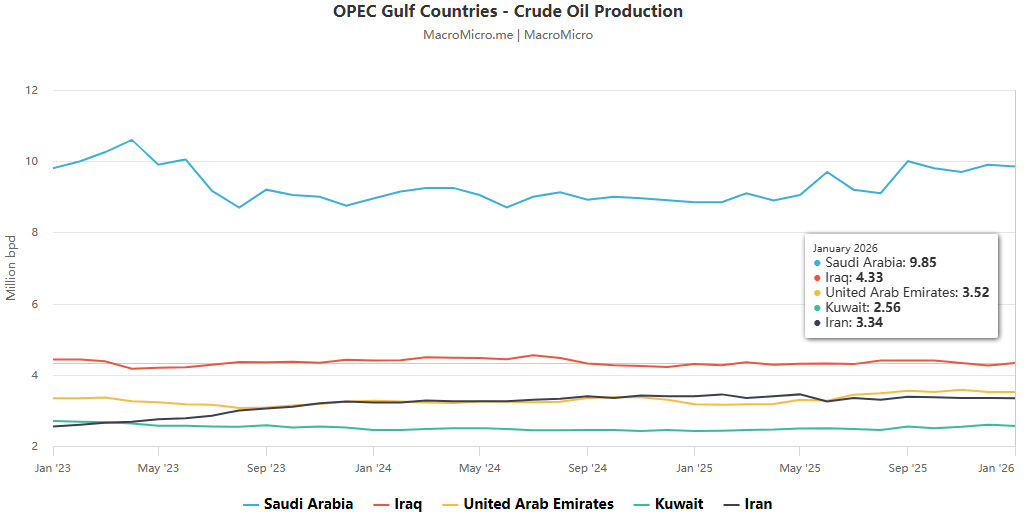

The stagnation of shipping in the Strait of Hormuz has pushed the supply capacity of Middle Eastern oil-producing countries to its limit. ACE Markets' energy research team, in conjunction with leading international institutions, has calculated and verified that if the strait were completely closed, the onshore storage capacity of the seven major Gulf oil-producing countries could only accommodate 22 days of retained production. Even with additional storage space on tankers, production could only be sustained for a maximum of 25 days; beyond that, a forced shutdown would be imposed. Alternative pipelines used by countries like Saudi Arabia and the UAE have limited capacity and cannot fill the core supply gap.

Combining institutional forecasts with its own supply and demand models, ACE Markets has developed three scenarios for oil price assessments:

Baseline scenario: The conflict eases within 1-2 weeks, and Brent crude oil prices remain in the range of $80-90 per barrel;

Moderate risk scenario: Regional energy infrastructure is attacked, and oil prices rise to $120 per barrel; probability of occurrence is approximately 20%.

Extreme risk scenario: If the disruption in the Taiwan Strait lasts for more than several weeks, oil prices will likely exceed $100 per barrel, and the hedging effect of OPEC+ production increases will be extremely limited.

Meanwhile, the platform's calculations and verifications show that the current oil price has already factored in a risk premium of approximately $18 per barrel, which is consistent with the impact of the six-week complete suspension of the strait's passage. Approximately 9% of the world's diesel and 18% of its jet fuel supply rely on the passage through this strait, and the volatility risk of related refining products needs to be monitored simultaneously.

III. Chain Reaction in the LNG Market: Increased Risk of Soaring Gas Prices in Europe and Asia

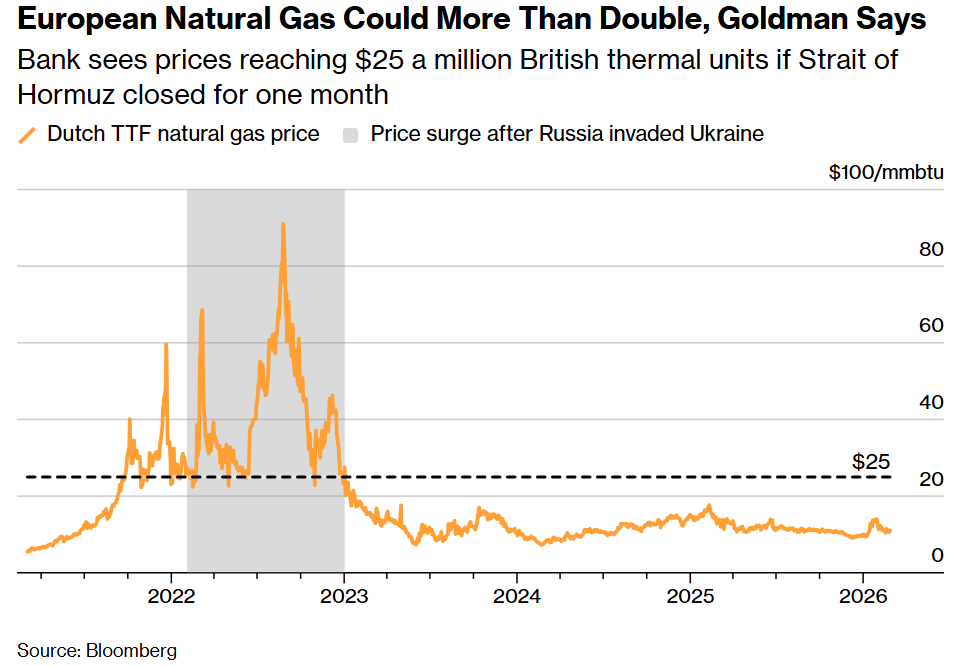

Compared to the crude oil market, the global LNG market is more dependent on the Strait of Hormuz, and the ripple effects of shipping disruptions are already beginning to emerge. ACE Markets' global natural gas market monitoring system shows that current benchmark natural gas prices in Europe and Asia barely factor in the risk premium related to Iran, indicating a severe under-preparation for the price shocks from a Strait disruption. This assessment aligns closely with the latest views from Goldman Sachs' energy research team.

Platform supply and demand models calculate that if LNG transport across the Taiwan Strait is disrupted for one month, Eurasian natural gas prices will surge by 130% to $25 per million British thermal units (MMBtu); if the disruption exceeds two months, European TTF natural gas prices will exceed €100 per megawatt-hour, triggering a disruption in global natural gas demand. In terms of regional impact, Europe and Asia are the core affected regions, as Qatar's LNG exports mainly flow to these two markets, and a disruption across the Strait will directly cut off their core supply. The United States, as the world's largest net LNG exporter, has liquefaction plants operating at full capacity for extended periods, leaving virtually no room for additional production to fill the gap.

IV. In-depth analysis: Short-term volatility intensifies, but the probability of a full-blown energy shock is limited.

ACE Markets, through cross-validation of multi-dimensional data, believes that the impact of this event on the energy market will be mainly short-term fluctuations, rather than a historic full-blown shock. Multiple buffering factors will significantly reduce the probability of the crisis spiraling out of control.

The conflict boundary is controllable: To date, neither side has launched attacks on core energy infrastructure such as oil fields, refineries, and export terminals. Iran has not weaponized oil and has not touched the core of the global energy supply chain.

The market landscape has fundamentally changed: the US shale gas revolution has significantly enhanced the ability to regulate oil prices, and the upper limit of market expectations for rising oil prices is significantly lower than the historical crisis highs, which will not trigger a global economic recession-level shock.

The market has a sufficient safety cushion: crude oil inventories had been replenished at low levels before the conflict, the Northern Hemisphere entered the off-season for energy demand, Asian buyers have sufficient strategic reserves, Western countries can stabilize prices by releasing strategic reserves, and the market has already priced in some of the risks.

Additional supply buffer: Rising oil prices will increase market demand for Russian crude oil subject to sanctions. If Western countries moderately ease restrictions, buyers such as India will increase their purchases, which could effectively alleviate the global supply gap.

V. Market Outlook and Key Monitoring Guidelines

According to ACE Markets' comprehensive analysis, the future course of the Middle East conflict and the pace of recovery of shipping in the Strait of Hormuz are the core variables determining the trend of the global energy market. In the short term, risk aversion and supply concerns will continue to drive up energy price volatility; if the conflict is prolonged and shipping in the Strait of Hormuz remains disrupted, the global energy supply chain will face a systemic shock, thereby pushing up global inflation and affecting the pace of monetary policy of central banks around the world.

The platform advises market participants to closely monitor three key signals: first, Iran's subsequent retaliatory actions, including whether they will target energy facilities or shipping in the Strait of Hormuz; second, the recovery of shipping traffic in the Strait of Hormuz and changes in the risk appetite of shipowners and insurance companies; and third, global responses, including the release of strategic reserves, OPEC+ production adjustments, and a loosening of policies regarding Russian crude oil. Investors can use ACE Markets' real-time commodity market data system and geopolitical risk alerts to stay informed about the situation and market changes.

The content of this article is spontaneously contributed by Internet users, and the views expressed in this article only represent the author himself. This website only provides information storage space services, does not own ownership, and does not assume relevant legal responsibilities.https://www.aneimedzi.cn/html/357.html